In this episode, we tackle the one question every U.S. homeowner eventually asks: how do people actually afford major home renovations? You see the beautiful kitchens and additions on TV, but nobody talks about the messy financial reality. The median cost for a major kitchen remodel now sits in the $75,000 to $150,000 range nationally, and that number can climb fast. Of course, a cosmetic refresh in a condo can start lower, but for a full gut job, the numbers are serious. We're going to break down the real math homeowners use, from HELOCs to phased construction, to turn a plan on paper into a finished space that passes final inspection.

What This Episode Is About

If you take three things from this conversation, make it these:

- The 'all-in' number is always higher than the contractor's bid. We'll cover the soft costs, contingency funds, and financing fees that most first-timers forget to include in their budget.

- Your financing choice dictates your project's timeline and flexibility. A Home Equity Line of Credit (HELOC) works very differently from a construction loan, and picking the wrong one can stall your project before the rough-in is done.

- Phasing the work is a valid strategy, but only if planned from day one. You can't just stop a project halfway. A smart phased approach plans the full load path and utility runs upfront, even if you only build the first part now.

The Real Numbers (National Picture)

Let's talk dollars. When you ask how to afford home renovation, the answer starts with knowing the real costs. According to the 2026 Cost vs. Value report from Remodeling Magazine, a mid-range major kitchen remodel has a national average cost of around $80,000, while an upscale one can easily exceed $155,000. A primary suite addition often lands between $175,000 and $350,000. These are just averages. Costs in dense coastal metros can be thirty to forty percent higher than in the Midwest or South. Why the big spread? Labor. Labor costs vary widely, driven by data from sources like the U.S. Bureau of Labor Statistics' Occupational Employment and Wage Statistics program, which provides granular data for different metropolitan statistical areas. Materials are a national market, but labor is always local.

To make this concrete, here are three representative projects from 2026, scoped similarly, reconstructed from Renology's Project of the Day network and used here in aggregate form:

- A 200-square-foot kitchen gut remodel in a suburban area: $92,000. This included semi-custom cabinets, quartz countertops, new appliances, and moving a non-load-bearing wall. The project was financed with a home equity loan.

- A primary bathroom addition (100 square feet) in a mid-sized city: $115,000. This involved a new foundation, framing, and tying into existing plumbing and electrical. The homeowner used a cash-out refinance on their mortgage.

- A full second-story addition (750 square feet) in a high-cost metro: $450,000. This was a complex job requiring significant structural work on the main floor to support the new load path. This was funded by a dedicated construction loan.

What Most Homeowners Get Wrong About This

The single biggest mistake is confusing the contractor's estimate with the total project cost. The bid you sign covers labor and materials for the defined scope of work. It does not cover everything. Homeowners get blindsided by three things: soft costs, change orders, and hidden conditions.

Soft costs include architectural plans, structural engineering reports, permit fees, and financing costs. These can add five to fifteen percent to your budget before a single hammer swings. Change orders are any deviation from the plan after the scope-lock date. Want a different tile? Want to add a window? That's a change order, and it comes with a price for both materials and schedule delay. Finally, hidden conditions are the nasty surprises inside your walls. Think knob-and-tube remnants in 1960s Tudors or galvanized supply lines in pre-1985 homes that crumble when you touch them. You won't know until demolition starts. This is why a contingency fund isn't optional. The National Association of Home Builders recommends a ten to fifteen percent contingency on renovations in homes over thirty years old. It’s the most important line item in your budget. For instance, a homeowner in a high-cost area like Sherman Oaks in Los Angeles or Lincoln Park in Chicago will face different math than someone in a lower-cost metro. The regional risks also change, from seismic retrofitting in places like Eagle Rock to managing deep frost lines in the Northeast.

The 3 Questions Every Homeowner Should Ask

3 pros, editor-screened. 4 questions.

See my 3 matchesBefore you call a single contractor or lender, you need to have a meeting with yourself and your finances. Get clear answers to these three questions. It will save you time, money, and a lot of stress.

- What is my 'walk-away' number? This is the absolute maximum you are willing to spend, including the contingency fund. Why it matters: This number anchors your entire project and prevents emotional decisions from blowing up your finances. What a good answer sounds like: "Our all-in budget is $120,000. That means a construction contract of no more than $105,000, leaving a $15,000 contingency we will not touch unless a structural or safety issue is discovered."

- Is this renovation for me, or for resale? You can't have it both ways. A project optimized for your specific taste may not appeal to future buyers. Why it matters: This defines your material choices and scope. High-ROI projects stick to neutral, high-quality finishes. Personal projects can indulge in that custom tile you love. What a good answer sounds like: "We plan to be here for at least ten years. This is for us. We want the durable, functional kitchen we've always dreamed of, and we're less concerned with recouping every dollar at sale."

- Can the house handle this scope? Your ambition needs to meet the reality of your home's structure. You can't put a 500-pound cast iron tub on floor joists sized for a fiberglass shower. Why it matters: Ignoring your home's existing load paths and utility capacity leads to massive, unbudgeted costs. What a good answer sounds like: "We're bringing in a structural engineer for a consultation before we even hire an architect. We need to know if our foundation and framing can support a second story before we spend money designing it."

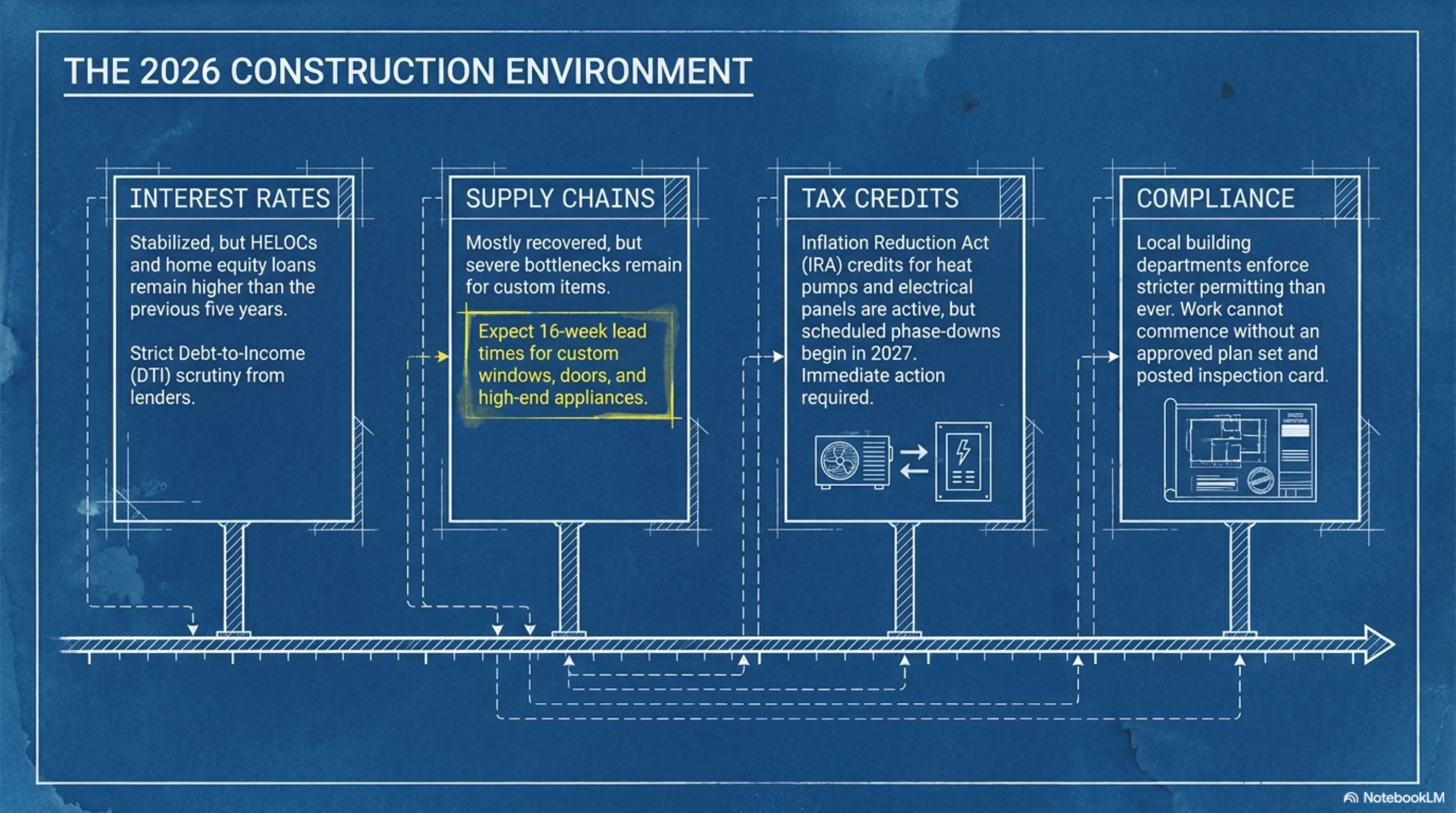

What Changed in 2026

The financial landscape for renovations is always shifting. In 2026, we're seeing a few key trends. First, the interest rate environment has stabilized, but rates for HELOCs and home equity loans remain higher than they were five years ago. This makes cash-out refinancing a less attractive option for homeowners with low-rate primary mortgages. Lenders are looking more closely at debt-to-income ratios, so having your financial house in order is critical before you apply. Second, material supply chains have mostly recovered from the pandemic whiplash, but lead times for custom windows, doors, and high-end appliances can still stretch to sixteen weeks. You have to order these items the moment your plans are finalized. Third, many of the federal tax credits from the Inflation Reduction Act for energy-efficient upgrades like heat pumps and electrical panel upgrades are still available, but with phase-downs scheduled for 2027 and beyond. If you're planning these upgrades, now is the time to act. Finally, local building departments are stricter than ever about proper permitting. Understanding the process before you start is critical. You can get a primer in our national home renovation permit playbook for 2026. Don't even think about starting work before you have an approved set of plans and your inspection card is posted.

The Renology Take

Here's the bottom line. Money doesn't build a project. A clear, detailed scope of work builds a project. The money just fuels it. The homeowners who succeed financially are the ones who spend more time on planning than they do on demolition. They resist the urge to 'figure it out as they go.' Get the scope locked before you pull a permit, and you'll stay in control of the budget. A loose scope is a blank check, and the house always cashes it. Don't start a project with a question mark on the budget. Start it with a period. This is the plan. This is the cost. This is the timeline. That's how you build with confidence. That’s how you actually afford it.

Sources & Methodology

See the Renology Methodology for how sources are reviewed, ranges are normalized, and planning-data limits are handled.

- Remodeling Magazine: 2026 Cost vs. Value Report

- National Association of Home Builders (NAHB): Remodeling Market Index (RMI), Q1 2026

- National Kitchen & Bath Association (NKBA): 2026 Design Trends Report

- U.S. Census Bureau: American Housing Survey (AHS)

- U.S. Bureau of Labor Statistics (BLS): Occupational Employment and Wage Statistics (OEWS)

- U.S. Department of Energy: Energy Star Program & Inflation Reduction Act Guidelines

- Renology Editorial Methodology: Project costs and timelines are synthesized from our network of contractor data and public permit records, reflecting market conditions as of Q2 2026.

Get 3 renovation bids in 48 hours.

Our editors already vetted contractors. Answer 4 questions and we send 3 written bids inside 48 hours, with the real price for your scope, not their inflated first-call number.

- Free, no commission

- Pre-screened locally

- Bids inside 48 hours

Takes about 60 seconds. We'll text you when bids arrive.