In this episode, I'm tackling the single biggest deferred maintenance item for any homeowner: the roof. Everyone asks, "Will my insurance cover it?" The short answer is almost always no. Insurance covers sudden, accidental damage, not a roof that's simply worn out. The average homeowner spends between $8,000 and $22,000 on a new roof, a cost that catches most people by surprise. I'm going to walk you through the real numbers, what most people get wrong about their coverage, and how to budget for the roof that insurance will not cover, so you're not caught scrambling when the first leak appears.

What This Episode Is About

If you take three things from this episode, make them these:

- Insurance Isn't a Maintenance Plan: Your homeowner's policy covers storm damage, not a roof that's failed from old age. I'll explain the difference and why you need a separate savings plan.

- The Underlayment Is the Real Roof: Shingles are just the armor. The weather barrier and solid decking underneath are what keep you dry. A cheap job that ignores what's underneath is just a waste of money.

- Cost Is More Than Shingles: The total roof replacement cost includes tear-off, disposal, decking repairs, flashing, ventilation, and labor. I'll break down the line items so you can understand any quote.

Nationally, the roof replacement cost for a typical 2,000-square-foot home using asphalt shingles ranges from $8,000 to $16,000 in 2026. The U.S. median cost is around $12,500. Costs can climb over $30,000 for premium materials like standing seam metal or tile on more complex rooflines.

The Real Numbers (National Picture)

Let's get down to the brass tacks. The final price on your contract is a function of three things: materials, labor, and the complexity of your roof. A simple gable roof is straightforward. A complex roof with dormers, valleys, and steep pitches requires more skill and time. These figures can start lower for a small townhouse or a simple re-shingle job, but for a full tear-off and replacement, the numbers get real, fast. Labor is the big variable. To give you a concrete example, prevailing wage data from the California Department of Industrial Relations for Los Angeles County shows certified roofers earn a premium, driving up costs in that market compared to a rural area in the Midwest.

Three representative projects from 2026, scoped similarly, reconstructed from Renology's Project of the Day network and used here in aggregate form:

- Basic Asphalt Shingle (3-Tab): On a 1,800 sq. ft. ranch house with a simple roofline. This is your entry-level, 20-year roof. Expect a roof replacement cost of $8,500 to $13,000.

- Architectural Asphalt Shingle (Most Common): On a 2,500 sq. ft. two-story home. This is the 30-year standard for most of the country. The cost runs from $12,000 to $19,000. This is where most projects land.

- Standing Seam Metal: On a 2,200 sq. ft. modern home. This is a 50-plus year roof system. The upfront investment is significant, typically $25,000 to $40,000, but the lifecycle cost can pencil out.

Remember to account for surprises. Once we tear off the old roof, we might find rotten decking. The National Association of Home Builders recommends a ten to fifteen percent contingency on renovations in homes over thirty years old. For a $15,000 roof, that's another $1,500 to $2,250 set aside for the unexpected.

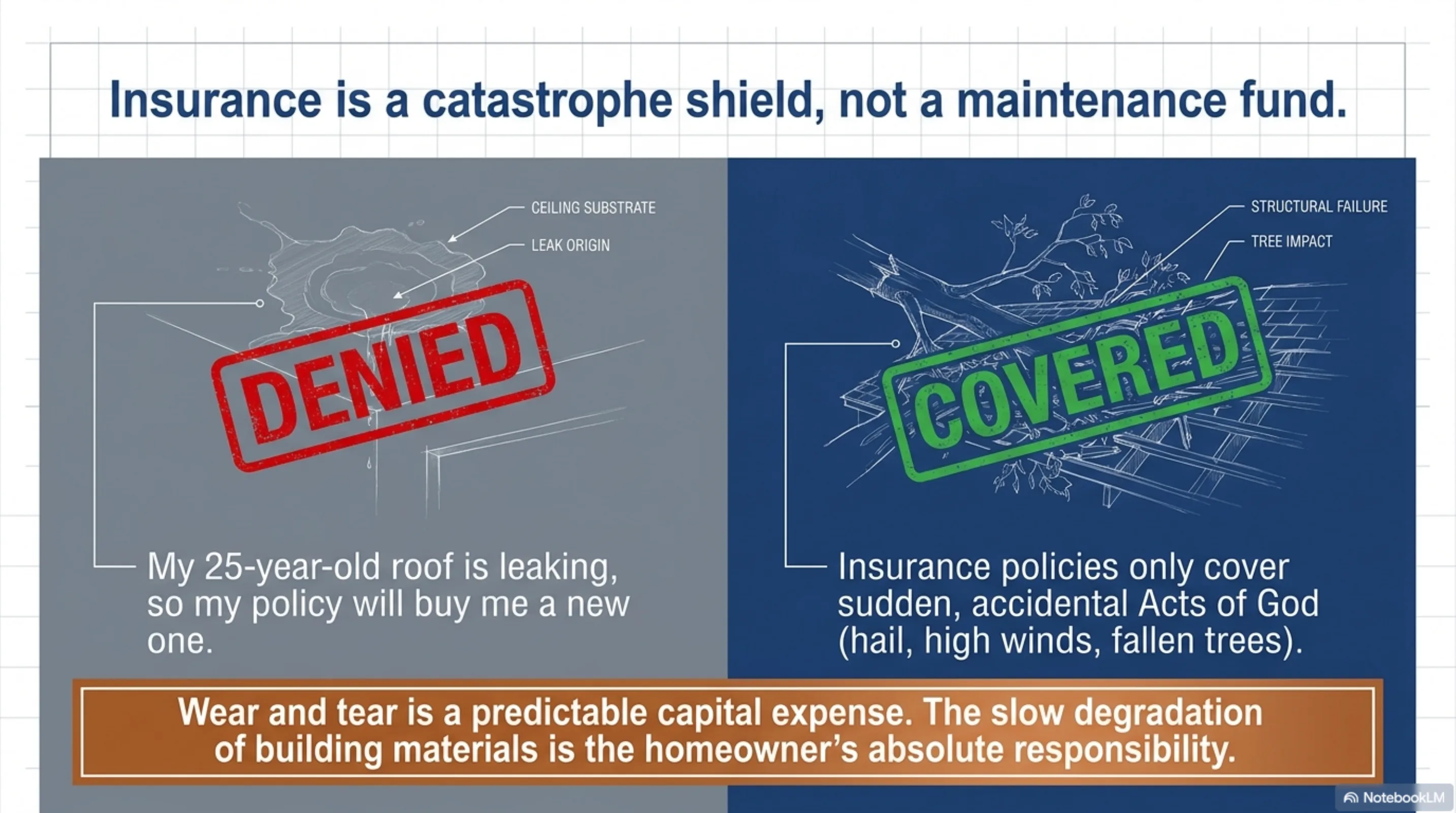

What Most Homeowners Get Wrong About This

The most common call I get is from a homeowner whose insurance claim was denied. They see a watermark on the ceiling and assume their policy will pay for a new roof. That's a fundamental misunderstanding of what insurance is for. It's for sudden, catastrophic events, what adjusters call an "Act of God." Think hail storms, high winds that rip shingles off, or a tree falling on your house. It is not for a 25-year-old asphalt roof that's shedding granules and cracking from a quarter-century of sun and weather.

Here's what you need to understand:

- Wear and Tear is Your Responsibility: The slow, predictable degradation of building materials is a homeowner's maintenance responsibility. It's a capital expense you have to plan for, just like a new furnace or water heater.

- Insurers Look for "Functional Damage": After a storm, an adjuster is looking for damage that compromises the roof's ability to shed water. A few dents in a metal roof might be cosmetic, not functional, and may not be covered.

- Policies Are Getting Stricter: In states with heavy storm activity, many carriers will no longer insure roofs over 15 or 20 years old, or they will only offer "Actual Cash Value" (ACV) coverage, which pays you for the depreciated value of your old roof, not the full cost of a new one.

Thinking your policy is a roof savings account is the fastest way to get into financial trouble. You need a real one. You can learn more about how to pay for these projects in our guide to financing home improvements.

The 3 Questions Every Homeowner Should Ask

3 pros, editor-screened. 4 questions.

See my 3 matchesWhen you get quotes, you need to ask the right questions to separate the pros from the chuck-in-a-truck crews. Don't just focus on the final price. Focus on the scope of work. A cheap bid that cuts corners will fail in five years. Any good contractor can answer these easily.

1. How will you assess my roof decking?

Why it matters: The plywood or OSB sheathing under your shingles is the structural foundation of your roof. Nailing new shingles into soft, rotten wood is a guaranteed failure. The load path is compromised. What a good answer sounds like: "We include replacing up to three sheets of decking in our standard price. If we find more extensive damage after tear-off, we'll stop, show you the issue, and approve a change order with you before proceeding. We can't know for sure until we see what's under there."

2. What is your detailed plan for flashing, valleys, and ventilation?

Why it matters: Leaks don't happen in the middle of the roof. They happen at penetrations: chimneys, skylights, vents, and where roof planes meet. This is where craftsmanship counts. What a good answer sounds like: "We replace all pipe boot flashing and install new step flashing and counter-flashing at all walls and the chimney. We use ice and water shield in all valleys and at the eaves. We'll also calculate your attic's ventilation needs to ensure you have a balanced intake and exhaust system to meet code."

3. Who is pulling the permit and managing inspections?

Why it matters: A roof replacement is structural work and requires a permit in almost every jurisdiction. The contractor, not the homeowner, should be responsible for this. An unpermitted job can cause major problems when you sell your home. What a good answer sounds like: "We handle everything. We'll pull the permit, post the inspection card, and schedule the mid-roof and final inspections with the city building department. You won't have to do a thing." Your contractor should manage this, but you can learn the process in our national roof replacement permit playbook for 2026.

What Changed in 2026

The roofing landscape is always shifting. What was true in 2024 has evolved. First, the rate environment. With interest rates holding steady at higher levels, financing a major project like a roof with a HELOC or home improvement loan is more expensive than it was a few years ago. This makes saving and budgeting ahead of time even more critical.

Second, material costs have stabilized for common products like asphalt shingles, but lead times for specialty products can still be unpredictable. If you want specific metal panels or imported tile, order them months in advance of your project's start date. A reputable contractor will guide you through this process. You can find one in our network of vetted local professionals.

Third, the federal Energy Efficient Home Improvement Credit is still a factor. Under the Inflation Reduction Act, you can claim a tax credit for 30% of the cost, up to $1,200, for qualifying energy-efficient roofing materials. Ask your contractor for products that meet the ENERGY STAR requirements.

Finally, building codes continue to get stricter, especially in areas prone to extreme weather. In hail-prone regions, impact-resistant shingles are becoming the standard. In high-wind coastal zones, enhanced nailing patterns are now mandatory. And in wildfire-prone states like California, codes now require Class A fire-rated roofing systems and specific attic venting to create defensible space. A roof in a high-risk area like the Hollywood Hills has different code requirements than one in a low-risk suburban area.

The Renology Take

I've been on thousands of roofs, from brand new construction to century-old homes. The meta-pattern I see is simple: homeowners treat their roof as a passive component until it fails. This is a mistake. Your roof is an active system that protects every other asset in your house. Deferring a $15,000 roof replacement for three years can easily lead to a $30,000 project once you account for replacing insulation, drywall, and framing from water damage. Don't think of it as an expense. It's a capital investment in the integrity of your home. Budget for it like one. A roof that doesn't leak isn't a luxury. It's the bare minimum of a functional building envelope. That's the Renology take.

Sources & Methodology

See the Renology Methodology for how sources are reviewed, ranges are normalized, and planning-data limits are handled.

- Remodeling Magazine, 2026 Cost vs. Value Report

- National Association of Home Builders (NAHB), Housing Market Index, Q1 2026

- National Roofing Contractors Association (NRCA), Market Survey 2025-2026

- U.S. Bureau of Labor Statistics (BLS), Occupational Employment and Wage Statistics for Roofers, May 2025

- U.S. Census Bureau, American Housing Survey

- Internal Revenue Service, Energy Efficient Home Improvement Credit Guidance (IRA 2022)

- Renology editorial methodology for aggregating project cost data from our contractor network.

Get 3 roof bids in 48 hours.

Our editors already vetted roofers. Answer 4 questions and we send 3 written bids inside 48 hours, with the real price for your scope, not their inflated first-call number.

- Free, no commission

- Pre-screened locally

- Bids inside 48 hours

Takes about 60 seconds. We'll text you when bids arrive.