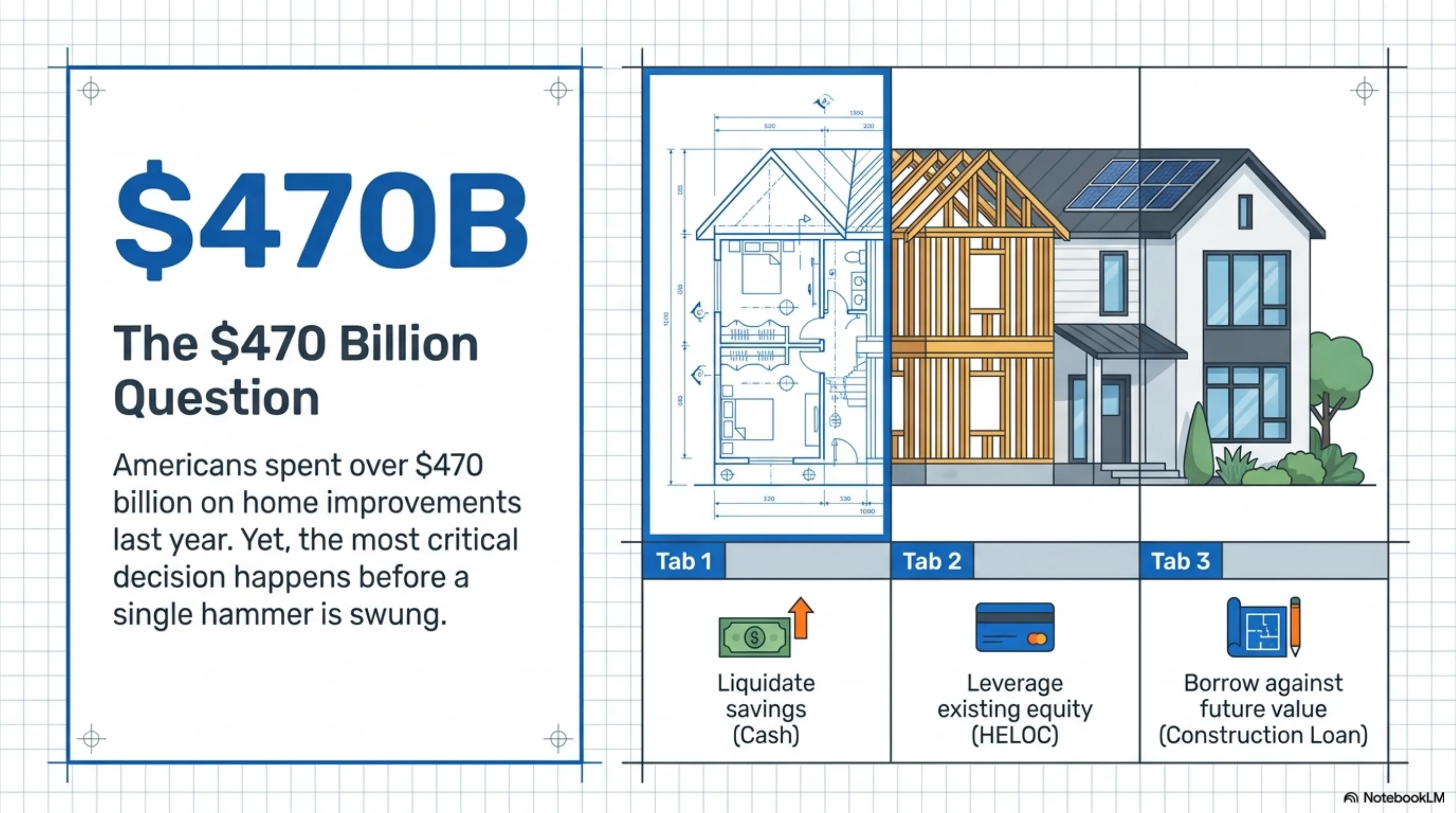

In this episode, we address the single most practical question every U.S. homeowner faces before a major renovation: how do I actually pay for it? According to the U.S. Census Bureau, homeowners spent over $470 billion on improvements last year. The debate often comes down to a construction loan vs HELOC, or simply paying with cash. Each path has distinct financial implications that are rarely explained clearly. A Home Equity Line of Credit (HELOC) leverages the equity you already have, offering flexibility. A construction loan finances the project itself in stages, based on its future value. In this episode, we break down the numbers, the risks, and the right questions to ask before you commit.

What This Episode Is About

In short, a Home Equity Line of Credit (HELOC) is a revolving line of credit against your existing home equity, best for projects with uncertain costs or multiple phases. A construction loan provides fixed funding in stages (draws) for a specific, large-scale project, with interest paid only on funds drawn. Cash provides the simplest path but eliminates your liquidity.

If you take three things from this episode, they should be:

- The True Cost of Money: We will itemize the total cost of borrowing for each financing type, including interest, closing costs, and appraisal fees, which are often omitted from initial quotes.

- Risk vs. Flexibility: You will learn how to map the project's scope to the right financing structure, balancing the fixed terms of a construction loan against the variable-rate risk of a HELOC.

- The 2026 Financial Picture: We will explain how the current interest rate environment and material cost stability affect the math for your renovation financing decision this year.

The Real Numbers (National Picture)

To understand the financing options, we first need to establish the scale of the cost. National data from Remodeling Magazine's 2026 Cost vs. Value Report provides a clear baseline for major projects. These figures represent the median contractor-led project costs across major U.S. markets. The lower end of these ranges typically applies to cosmetic updates in smaller homes or condos, while the upper end reflects structural changes or high-end finishes in larger single-family homes.

- Major Kitchen Remodel (Midrange): $78,500, $94,000. This includes new semi-custom cabinets, countertops, appliances, flooring, and lighting. This project typically recoups 55%, 65% of its cost at resale.

- Bathroom Remodel (Upscale): $79,000, $88,000. This involves expanding the space, relocating fixtures, adding a walk-in shower, a freestanding tub, and high-end finishes.

- Primary Suite Addition (Midrange): $165,000, $205,000. This covers a 24x16-foot addition with a full bathroom and walk-in closet.

- ADU Conversion (Garage): $150,000, $225,000. Converting an existing two-car garage into a living unit with a kitchen and bathroom. You can find more detail in our guide to ADU costs.

Three representative projects from 2026, scoped similarly, reconstructed from Renology's Project of the Day network and used here in aggregate form:

- Project 1 (Cash): A $92,000 kitchen remodel paid from savings. The project was completed two weeks ahead of schedule because funding was never a bottleneck.

- Project 2 (HELOC): A $145,000 phased backyard and primary bathroom update. The homeowner drew funds as needed over nine months, paying interest only on the $110,000 used.

- Project 3 (Construction Loan): A $380,000 second-story addition. The funds were disbursed in five draws after inspections, protecting the homeowner from paying for incomplete work.

Construction Loan vs. HELOC vs. Cash: A Detailed Comparison

Choosing how to fund a project is as critical as choosing a contractor. Each method has a different structure, cost profile, and risk level. The correct choice depends on your project's scale, your timeline, and your personal balance sheet.

Construction Loans

A construction loan is short-term financing designed specifically for building something new, whether it's a ground-up home or a major addition. Unlike a mortgage, the funds are not paid in a lump sum. Instead, the lender releases money in stages, or “draws,” as the project hits pre-approved milestones (e.g., foundation poured, framing complete). The loan is typically interest-only during the construction phase. Once the project is finished, it's either converted into a traditional mortgage or paid off. The loan amount is based on the appraised value of the home *after* the renovation is complete.

- Pros: Allows you to fund projects that exceed your available cash or home equity. The draw schedule protects you from paying for work that hasn't been completed to standard.

- Cons: The process is complex, with more paperwork, inspections, and higher closing costs ($3,000, $6,000) than other options. Interest rates are typically 1%, 2% higher than standard mortgage rates.

Home Equity Line of Credit (HELOC)

A HELOC is a revolving line of credit that uses your home as collateral. It functions like a credit card: you are approved for a certain limit and can borrow, repay, and re-borrow funds as needed for a set period (the “draw period,” usually ten years). You only pay interest on the amount you’ve borrowed. A HELOC requires you to have significant existing equity in your home, as lenders typically allow you to borrow up to 85% of your home's value, minus your outstanding mortgage balance. For more on this, see our bathroom remodel cost guide.

- Pros: Offers great flexibility for projects with uncertain timelines or costs. Closing costs are low, sometimes zero. Interest paid may be tax-deductible if used for home improvements.

- Cons: Most HELOCs have variable interest rates, meaning your monthly payment can change. Using your home as collateral puts it at risk if you cannot make payments.

Paying with Cash

Using cash from savings is the most straightforward financing method. It involves no lenders, no interest payments, and no debt. This path gives you maximum control and simplifies the renovation process, as there are no draw schedules or appraisals to coordinate. It is the financially optimal choice if, and only if, you can afford the entire project without depleting your emergency fund or compromising other financial goals.

- Pros: No interest costs, no loan application process, and no monthly payments. You have total control over the funds and project timeline.

- Cons: Depletes liquid savings, which could be needed for emergencies. There is an opportunity cost, as those funds could have been generating returns elsewhere. Large projects can easily exceed initial cash reserves.

What Most Homeowners Get Wrong About This

3 pros, editor-screened. 4 questions.

See my 3 matchesThe most common misconception is that the contractor's bid represents the total project cost. This is seldom true. The bid covers direct costs: labor and materials. It almost never includes the indirect costs, which can add 20% to 30% to the final amount. Homeowners who budget based only on the quote often find themselves short on funds mid-project.

Here are the three costs most often overlooked:

- Financing Costs: Loan origination fees, appraisal fees, title insurance, and interest payments during construction are real costs. For a $150,000 construction loan, these can amount to $5,000, $9,000 before the project even breaks ground.

- Soft Costs: These include fees for architects or designers ($5,000, $15,000 on a major remodel), structural engineers, and building permits, which can run from $1,000 to $4,000 depending on project scope.

- Contingency Fund: Unexpected issues always arise, from finding outdated wiring to dealing with rotted framing. The National Association of Home Builders recommends a ten to fifteen percent contingency on renovations in homes over thirty years old. For a $100,000 project, that is an extra $10,000 to $15,000 you need to have available.

Failing to budget for these three categories is the primary reason projects go over budget and stall before completion.

The 3 Questions Every Homeowner Should Ask

Before you sign any loan documents or write the first check, you need clear answers to three fundamental questions. Posing these to your lender and your contractor will expose gaps in your plan and prevent costly surprises down the road.

1. What is the all-in cost, including fees, interest, and contingency?

- Why this matters: This question forces a shift from the contractor's bid to the total capital required. It accounts for borrowing costs and the inevitable project overruns, providing a realistic final number.

- What a good answer sounds like: "The project bid is $120,000. We recommend a 15% contingency of $18,000. Loan fees and closing costs are $4,500. Your total required funding is $142,500."

2. What is the detailed draw schedule and inspection process?

- Why this matters: For construction loans, this defines project milestones and when you pay for them. A clear schedule tied to inspections protects you from paying for substandard or incomplete work. You can learn more about this in our national remodeling permit playbook.

- What a good answer sounds like: "We will have five draws. The first is 10% after permits are issued. The second is 25% after framing and rough-ins pass city inspection. Each subsequent draw requires an inspection and lien waiver from all subcontractors."

3. How does this project's cost compare to its resale value?

- Why this matters: This frames the project as a financial decision, not just a lifestyle upgrade. Knowing the potential return on investment helps prioritize spending and avoid over-improving for your market.

- What a good answer sounds like: "Based on the 2026 Cost vs. Value report, a kitchen remodel of this scope costs a median of $85,000 and adds approximately $51,000 in resale value, for a 60% cost recovery."

What Changed in 2026

The financial environment for home renovations has shifted since the volatility of the early 2020s. For homeowners planning projects in 2026, three factors are paramount. First, interest rates have stabilized. After years of fluctuation, HELOC and construction loan rates are now holding in a more predictable range of 6.0% to 8.5%, according to Federal Reserve data. This stability allows for more accurate long-term budget forecasting.

Second, material cost inflation has cooled. The supply chain disruptions that caused lumber and steel prices to spike have largely resolved. The Producer Price Index for construction materials shows only a modest 1.5% to 2.5% increase over the last twelve months, compared to double-digit growth in previous years. However, labor costs continue to rise. Bureau of Labor Statistics (BLS) data shows construction wages are up 4.5% to 5.5% year-over-year due to persistent skilled labor shortages.

Finally, federal incentives like the Inflation Reduction Act (IRA) continue to influence project scope. Tax credits for high-efficiency windows, heat pumps, and electrical panel upgrades can offset costs by up to 30%, making these energy-focused updates more financially attractive than ever before.

The Renology Take

The central mistake homeowners make is choosing a financing product based on a single variable, usually the interest rate. The real analysis in the construction loan vs HELOC debate is about matching the financial tool to the job. A construction loan is a structured, purpose-built tool for a large, well-defined project. It imposes discipline. A HELOC is a flexible, multi-purpose tool, ideal for phased projects with evolving scopes. Cash is simplest but carries the highest liquidity risk.

The meta-pattern we see is a failure to align the financing timeline with the project timeline. An eighteen-month addition funded by a twelve-month interest-only loan creates a payment shock. A five-year HELOC draw period for a project that takes six months means carrying an open credit line unnecessarily. The right choice is the one where the cost, terms, and structure of the loan map directly to the scope and duration of the work. That is the key to affordability.

Sources & Methodology

See the Renology Methodology for how sources are reviewed, ranges are normalized, and planning-data limits are handled.

- Remodeling Magazine: 2026 Cost vs. Value Report. National and regional data on project costs and resale values.

- National Association of Home Builders (NAHB): Remodeling Market Index (RMI), Q1 2026. Data on market sentiment and contractor-reported project costs.

- U.S. Census Bureau: Annual Capital Expenditures Survey (ACES), 2025. Data on national spending for residential improvements.

- U.S. Bureau of Labor Statistics (BLS): Producer Price Index (PPI) for Construction Materials and Employment Cost Index (ECI), 2026. Data on material and labor cost trends.

- The Joint Center for Housing Studies of Harvard University: Improving America's Housing 2025 Report. Analysis of remodeling market drivers and trends.

- Federal Reserve Economic Data (FRED): Prime Loan Rate and Mortgage Rate data, 2026.

- Renology Editorial Methodology: Our cost estimates are synthesized from the sources above, alongside proprietary data from our network of general contractors and project cost data submitted by homeowners.

Get 3 renovation bids in 48 hours.

Our editors already vetted contractors. Answer 4 questions and we send 3 written bids inside 48 hours, with the real price for your scope, not their inflated first-call number.

- Free, no commission

- Pre-screened locally

- Bids inside 48 hours

Takes about 60 seconds. We'll text you when bids arrive.