In this episode, we are tackling the single biggest question every U.S. homeowner faces before starting a major renovation: How do I pay for this? With national data showing that nearly two-thirds of large projects are funded with home equity, the conversation quickly turns to a critical choice. This is the definitive showdown of home equity loan vs HELOC. We are not just talking about interest rates. We are talking about the fundamental structure of your financing and how it aligns with the reality of a six-month kitchen gut or a primary suite addition. We will explore which tool gives you the control you need in 2026.

What This Episode Is About

If you take three things away from our conversation today about funding your dream renovation, let them be these:

- The Core Difference: We will clarify the essential distinction between a home equity loan, which provides a predictable lump sum at a fixed rate, and a Home Equity Line of Credit (HELOC), which acts as a flexible, variable-rate credit card tied to your home.

- The 2026 Market Context: We will analyze how the current interest rate environment and construction market realities should influence your decision, moving beyond simple rate comparisons to a more complete project-based financial strategy.

- Matching the Tool to the Job: You will learn how to diagnose your own project's scope, timeline, and budget uncertainty to confidently choose the financing product that minimizes risk and maximizes your control over the outcome.

The Real Numbers (National Picture)

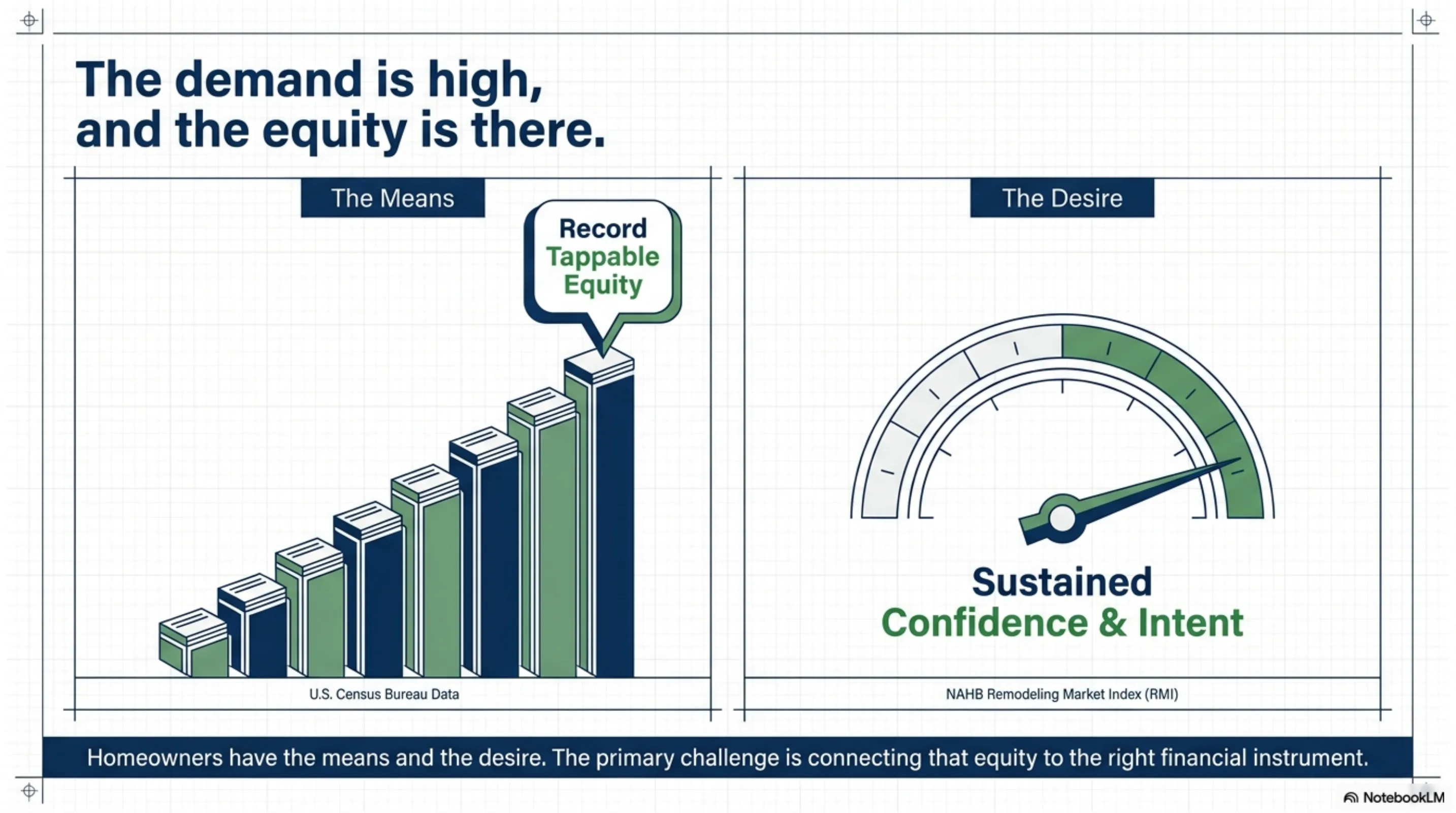

To ground our discussion, let's look at what renovations actually cost in 2026. According to the latest Remodeling Magazine Cost vs. Value Report, a midrange major kitchen remodel has a national average cost between $80,000 and $95,000. Stepping up to a midrange primary suite addition will see costs in the $160,000 to $190,000 range across most U.S. metros. Of course, these numbers can start lower for a cosmetic refresh or a smaller condo kitchen, but for a project involving layout changes and high-end finishes like honed quartzite countertops, this is the budget reality. So, where does the money come from? The U.S. Census Bureau's housing data confirms that American homeowners are sitting on a record amount of tappable home equity. The National Association of Home Builders' Remodeling Market Index remains strong, showing sustained confidence and intent from homeowners to invest in their properties. The demand is there, and the equity is there. The challenge is connecting them with the right financial instrument. The home equity loan vs HELOC debate is central to turning that equity into a functional, beautiful new space.

What Most Homeowners Get Wrong About This

The most common mistake homeowners make is believing the home equity loan vs HELOC decision is just a hunt for the lowest interest rate. Lenders prominently feature their rates, so it is an easy, tangible number to compare. But this focus misses the most important part of the story: project structure. The real choice is between budget predictability and project flexibility. One is not universally better than the other; they are simply different tools for different jobs. A home equity loan is for a project with a known, fixed cost. You receive the entire amount upfront, and your monthly payment is fixed for the life of the loan. It is the right choice when your contractor has given you a detailed, fixed-price contract for a defined scope. A HELOC, on the other hand, is built for projects with evolving scope or phased timelines. It is a revolving line of credit you draw from as needed, paying interest only on what you use. It is ideal when you might add scope later or when costs are not fully locked in. The decision boils down to three points:

- A locked scope of work points toward a home equity loan.

- An uncertain or phased scope points toward a HELOC.

- A low tolerance for payment changes favors the stability of a fixed-rate home equity loan.

The 3 Questions Every Homeowner Should Ask

3 pros, editor-screened. 4 questions.

See my 3 matchesBefore you speak to a lender, sit down with your project plans and ask these three questions. The answers will point you to the right financing product.

1. How certain is my total project budget?

Why this matters: This is the central question. It determines whether you need a single, predictable lump sum or ongoing, flexible access to funds. What a good answer sounds like: “We have a signed, fixed-price contract for $125,000, and our scope is completely locked. We know exactly what we need.” This certainty makes a home equity loan a perfect fit.

2. What is my personal tolerance for fluctuating monthly payments?

Why this matters: A HELOC’s variable interest rate means your payment can change. You need to be honest about whether your household budget can absorb potential increases. What a good answer sounds like: “I need to know that my payment will be the exact same amount every month for the next 15 years, regardless of what the market does.” This desire for stability points directly to a home equity loan.

3. Could my project expand or happen in multiple phases?

Why this matters: Renovations often uncover new needs, or you may plan to tackle the kitchen now and the landscape next year. A HELOC provides that built-in flexibility. What a good answer sounds like: “We are doing the addition now, but if we find issues with the old roof, we want the ability to address that without a new loan application.” This points to a HELOC.

What Changed in 2026

The landscape for financing a renovation has shifted since the early 2020s. In 2026, the interest rate environment has stabilized from the volatility of previous years, but rates remain higher than the historical lows we once saw. This new normal makes the fixed-rate certainty of a home equity loan particularly appealing for budget-conscious homeowners. Many are choosing to lock in a predictable payment rather than risk the potential upward drift of a HELOC’s variable rate. On the materials side, while general supply chains have improved, lead times for specialty items like custom rift-cut white oak cabinetry or high-performance European windows can still be unpredictable. These potential delays can extend a project's timeline, making a HELOC’s typical ten-year draw period a useful feature. Finally, the Inflation Reduction Act's tax credits for energy-efficiency upgrades are a major factor. Homeowners are bundling heat pump installations and electrical panel upgrades into their renovations, and both loan types are effective ways to finance these green additions before claiming the credit.

The Renology Take

From a designer’s perspective, the home equity loan vs HELOC debate is not about finance. It is about project management. Homeowners focus too much on the interest rate and not enough on the workflow of their renovation. The financing must match the project's structure. If your scope is locked, your materials are selected, and your contractor has given you a firm price, a home equity loan is your instrument. It is clean, predictable, and finite. You get your lump sum and build your project. But if your project is more fluid, perhaps a whole-house refresh where you are making decisions room by room, a HELOC is the superior tool. It provides the flexibility to match your spending to your evolving design choices. The one thing to remember is this: Finalize your scope of work first. Then, and only then, choose the financial product that perfectly fits that scope. I'm Sarah Chen for Renology. We'll see you on the next episode.

Sources & Methodology

See the Renology Methodology for how sources are reviewed, ranges are normalized, and planning-data limits are handled.

- Remodeling Magazine: 2026 Cost vs. Value Report

- National Association of Home Builders (NAHB), Remodeling Market Index, Q1 2026

- National Kitchen & Bath Association (NKBA), 2026 Design Trends Report

- U.S. Census Bureau, American Housing Survey, 2025 Data Release

- U.S. Bureau of Labor Statistics (BLS), Occupational Employment and Wage Statistics

- Internal Revenue Service, Publication 936, Home Mortgage Interest Deduction

- The Renology editorial team's methodology for national cost analysis, which synthesizes public and private construction data to establish representative project budgets.

Get 3 renovation bids in 48 hours.

Our editors already vetted contractors. Answer 4 questions and we send 3 written bids inside 48 hours, with the real price for your scope, not their inflated first-call number.

- Free, no commission

- Pre-screened locally

- Bids inside 48 hours

Takes about 60 seconds. We'll text you when bids arrive.